In recent weeks and months, we have been seeing pressure across grain and oilseed markets. Rapeseed markets especially have been feeling significant pressure.

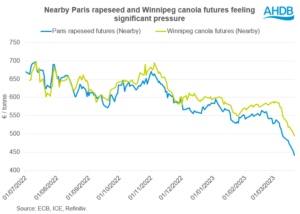

Since the start of March, Paris rapeseed (May-23) futures have lost €87.50/t (17%), to yesterday’s close at €441.00/t. The Winnipeg canola contract (May-23) has fallen by CAD$89.20/t (11%) over the same period, to close yesterday at CAD$729.40/t.

The discount of Paris rapeseed to Winnipeg canola continues to grow too.

So, what has been causing this pressure? According to Megan Hesketh, senior analyst, Arable, AHDB: “Fundamentally rapeseed is well supplied globally, and demand concerns rumble on for oil and vegetable oil markets, considering recessionary and financial market concerns globally.

“While we have seen support recently from Argentinian drought trimming the global soyabean outlook, and firming Chicago soyabean price levels, rapeseed prices have continued to fall. Following on from the mentioned well-supplied rapeseed global market, Australia’s record rapeseed crop continues to be offered on world market at a discount to other major origins . This is currently one of the key bearish factors weighing on rapeseed markets currently (oilworld.biz).”

“While we have seen support recently from Argentinian drought trimming the global soyabean outlook, and firming Chicago soyabean price levels, rapeseed prices have continued to fall. Following on from the mentioned well-supplied rapeseed global market, Australia’s record rapeseed crop continues to be offered on world market at a discount to other major origins . This is currently one of the key bearish factors weighing on rapeseed markets currently (oilworld.biz).”

Rape oil pressuring rapeseed prices

Another key element pressuring rapeseed prices is weakness in rapeseed oil (rape oil) markets.

Most vegetable oil prices overall recorded declines this month. Reasons for this are large stocks and large crushing of rapeseed and sunflowerseed, energy markets weakness as well as increased export supply from EU and Black Sea (oilworld.biz).

Rape oil prices especially have led the pressure in vegetable oil markets. Earlier this month rape oil fell lower than palm oil prices. This is significant as it is rare for another vegetable oil to fall below palm oil prices and reflects the bearish tone in the EU rape oil market currently. Especially since last year rape oil was at the ceiling of the vegetable oil complex. Though it is important to note that palm oil prices have felt some support from seasonal low production in top producing countries Malaysia and Indonesia (Dec-Feb/Mar).

Since late August 2022, soyabean oil has been at the ceiling of the vegetable oil complex, supported by trimmed soyabean production in Argentina as well as slower biodiesel production in Argentina and Brazil, keeping soyabean oil exports high (Oilworld.biz).

Will pressure continue?

“The EU is expected to have a rapeseed surplus by the end of the marketing season,” adds Ms Hesketh. “With a build up of stocks in Romania and Poland, due to exports from Ukraine. Australian rapeseed is very competitive into the EU, and rapeseed is in competition with sunflower and soyabeans at crush plants (Stratégie Grains). Especially with soyameal prices elevated on a smaller Argentinian soyabean crop.

“As a result, EU rapeseed stocks are expected to jump up this season. Looking ahead to next season, we are also expecting a large availability from harvest 2023. Therefore, rapeseed prices are expected to continue to feel pressure, short and longer term.

“Watchpoints remain Argentina’s soyabean crop, and how low forecasts can go. Additionally, as the La Niña changes to an El Niño, what impact might this have on Australian production next season? Finally, as low production phases end for palm oil in Malaysia and Indonesia, how much palm can we expect to enter the market? Things to consider.”